Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Every cycle hands contrarians the same temptation: wait for the miners to break, then back up the truck. The logic is seductive because it has worked before. When the people who literally manufacture the asset can no longer afford to keep the machines running, the marginal seller is exhausted, the float tightens, and price tends to find a floor. The problem with treating that as a mechanical buy signal in 2026 is that the conditions which made it reliable have quietly eroded, and the data this month says the squeeze is genuine but unfinished.

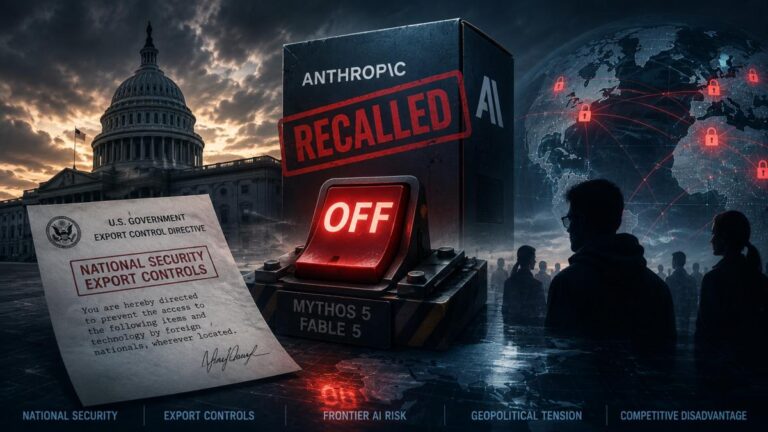

On a Friday evening in June, at precisely 5:21pm Eastern, the most valuable private company in artificial intelligence received a letter that rewrote the risk profile of the entire sector. The US government, invoking national security export controls, instructed Anthropic to bar every foreign national on earth from its two newest models. Because the order swept in the company's own non-citizen engineers, selective compliance was mechanically impossible. So Anthropic did the only thing the directive left open to it: it switched the models off for everyone, everywhere, three days after launch.

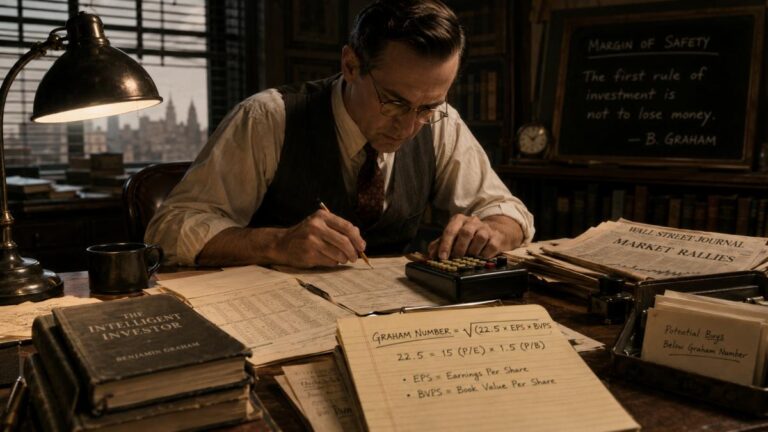

Picture an investor in the 1940s hunched over a set of financial statements, calculator in hand, hunting for the handful of stocks the crowd had ignored. Odds are that investor had absorbed the teachings of Benjamin Graham, the man most people credit as the founder of value investing. Graham distrusted enthusiasm. He built simple, almost stubbornly conservative rules to keep ordinary investors from overpaying, and one of those rules has outlived nearly every market regime since: the Graham Number.

There is a thesis making the rounds in every investment forum, every analyst note, and every infrastructure fund pitch deck right now, and it goes like this: the real AI trade is not chips, it is electrons. Data centres are devouring power. Grids cannot keep up. Therefore, buy everything that generates, transmits, or stores electricity, and wait.

Scroll through any investing forum right now and the word "bubble" arrives before the second sentence. The comparison writes itself: a narrow band of technology names dragging the entire index higher, valuations that make traditional metrics look quaint, and a chorus of skeptics pointing at the year 2000 as the obvious template. Yet beneath the noise sits a more interesting argument, one that retail and professional investors keep circling back to. What if the spending driving this rally is structurally different from the speculative excess that defined the dot-com mania? What if artificial intelligence capital expenditure behaves less like a luxury and more like a cost-cutting necessity that companies fund even when the economy turns?

Every few months a new headline declares that the solid-state battery, the so-called holy grail of energy storage, has finally arrived. The latest comes from Wuhan, where Dongfeng Motor says its 350 Wh/kg solid-state cell will reach mass production and vehicle integration in the second half of 2026, enabling driving ranges past 1,000 km. The specifications are genuinely impressive: cells that keep working after being crushed by 50 percent, that survive 170 degrees Celsius without smoke, and that retain over 74 percent of their charge at minus 30 degrees. For anyone tracking the EV supply chain, it is the kind of announcement that moves share prices.

A professor at Duke recently ran an experiment with his Silicon Valley class. He handed each student a bag of Skittles and set them loose: trade your way to a single-color hoard, and the biggest hoard of each color earns a free pass on a homework assignment. Twenty minutes, open-floor haggling, all the frantic strategy you would expect from ambitious students. Who's holding the reds? Should I dump my purples early? Can I trust the guy in the corner?

For most of its existence, the quantum threat to Bitcoin lived in the same mental drawer as alien contact and asteroid strikes: theoretically real, practically ignorable, and useful mostly for headlines. That drawer is now jammed open. Across the first half of 2026 a sequence of research papers, testnet deployments, and institutional warnings has shifted the conversation from whether Bitcoin needs to worry about quantum computing to whether it has left itself enough time to do anything about it. The honest answer is uncomfortable: the network can almost certainly be saved, but a meaningful slice of its supply may already be beyond saving.

On May 29, 2026, at 4:00 p.m. Central Time, a technical pattern that had defined Bitcoin trading since 2017 ceased to exist. The CME gap, one of the most reliably watched signals in all of crypto technical analysis, was not killed by a market crash or a regulatory ruling. It was killed by the logical conclusion of institutional adoption: the world's largest regulated derivatives exchange finally conceding that an asset trading 24 hours a day, seven days a week cannot be adequately served by a venue that closes for the weekend.

The "digital gold" narrative has been the load-bearing wall of Bitcoin's institutional investment thesis for the better part of a decade. The idea was elegant and easy to communicate: fixed supply, no central bank, immune to debasement, a hedge for the monetary chaos that fiat systems periodically produce. Sovereign wealth managers understood it. Family offices modelled it. Pension consultants used it to justify allocation. In 2026, the empirical data is dismantling it in real time, and the investors who are clearest about what is actually happening will be best positioned for what comes next.